Navigating the world of real estate investment can be both thrilling and daunting.

There are numerous financing options available, each with its own advantages and limitations.

When it comes to acquiring investment properties, understanding these loan types is crucial for making informed decisions. Our goal is to provide clarity on the primary loan types available for real estate investment properties.

In the realm of real estate investment, the financial structure is as pivotal as the property itself.

With the right financing in place, we can maximize potential returns while managing risks effectively.

Exploring the various loan options empowers us to align our investment strategies with our financial capabilities and long-term goals.

1) Conventional Loan

Conventional loans are popular for real estate investors.

These loans are not backed by government agencies but follow guidelines set by entities like Fannie Mae and Freddie Mac.

We often choose this option because it offers flexibility in terms and conditions.

Typically, a down payment is required.

Lenders generally ask for at least 15%, sometimes more, depending on the specific circumstances and property type.

Borrowers with higher credit scores might secure lower down payment requirements.

One advantage is the potential for lower interest rates.

By meeting the necessary credit and financial criteria, we can often negotiate favorable terms.

This boosts the overall return on our investment properties.

Conventional loans apply to various property types, including single-family homes, duplexes, and condos.

The maximum loan limits for these properties align with those for primary residences.

As of 2024, we can borrow up to $766,550 for a single-unit property in most areas.

Income stability and a good credit history are crucial for approval.

Lenders assess our financial profiles carefully, so maintaining strong financial health can be beneficial.

Successfully securing a conventional loan enhances our investment strategies.

Mortgage insurance is typically not required if our down payment is 20% or more.

This can save us money in the long run.

Conventional loans remain a strong choice for real estate investors looking to expand their portfolios.

2) Hard Money Loan

Hard money loans are short-term financing options often used by real estate investors looking to secure quick capital.

Unlike traditional loans, they are primarily based on the property’s value rather than the borrower’s creditworthiness.

These loans can be particularly useful for projects that require a fast turnaround or when a property is deemed less conventional or higher risk.

The interest rates on hard money loans are generally higher, typically ranging from 10% to 15%.

Lenders offer these higher rates to compensate for the increased risk they take on.

Repayment terms are usually shorter as well, often around one to five years.

This makes them suitable for investors who plan on quickly reselling the property.

Loan amounts often depend on a percentage of the property’s after-repair value (ARV).

This approach allows investors to finance both the purchase and the renovation costs.

Qualifying for a hard money loan involves criteria that differ by lender.

However, it usually revolves around the property’s value and potential, rather than personal financial history.

This type of loan can be beneficial for fix-and-flip strategies where speed and flexibility are critical.

It allows us to obtain funds swiftly and efficiently, potentially maximizing our investment returns.

While these loans provide many advantages for experienced investors, they may not suit everyone.

Evaluating the risks and potential returns is crucial before opting for a hard money loan.

3) FHA 203(k) Loan

When we think about purchasing a property that needs improvement, the FHA 203(k) loan often comes to mind.

This loan, insured by the Federal Housing Administration, offers a practical way for buyers to finance both the purchase of a home and its necessary repairs.

This loan targets those of us interested in buying properties that are considered “fixer-uppers.” By combining the costs of purchasing and renovating into one loan, it simplifies the financing process.

This could be a pivotal choice for investors looking to revamp older homes.

For our projects, the FHA 203(k) loan demands a credit score of at least 580 to qualify for the minimum 3.5% down payment.

Those with lower scores might see higher requirements.

Additionally, it’s crucial to note that the loan is reserved for primary residences, so it won’t fit every investment scenario.

We can use this loan to purchase multifamily units, provided we occupy one as our primary residence.

It’s the only way to leverage a 203(k) for what could be considered an investment property.

This stipulation aligns with FHA rules designed to encourage homeownership.

The loan also has limits, typically capping at a specified amount based on regional housing market trends.

We must consider this before setting our renovation ambitions too high.

It’s a cost-effective avenue, but comes with clear boundaries.

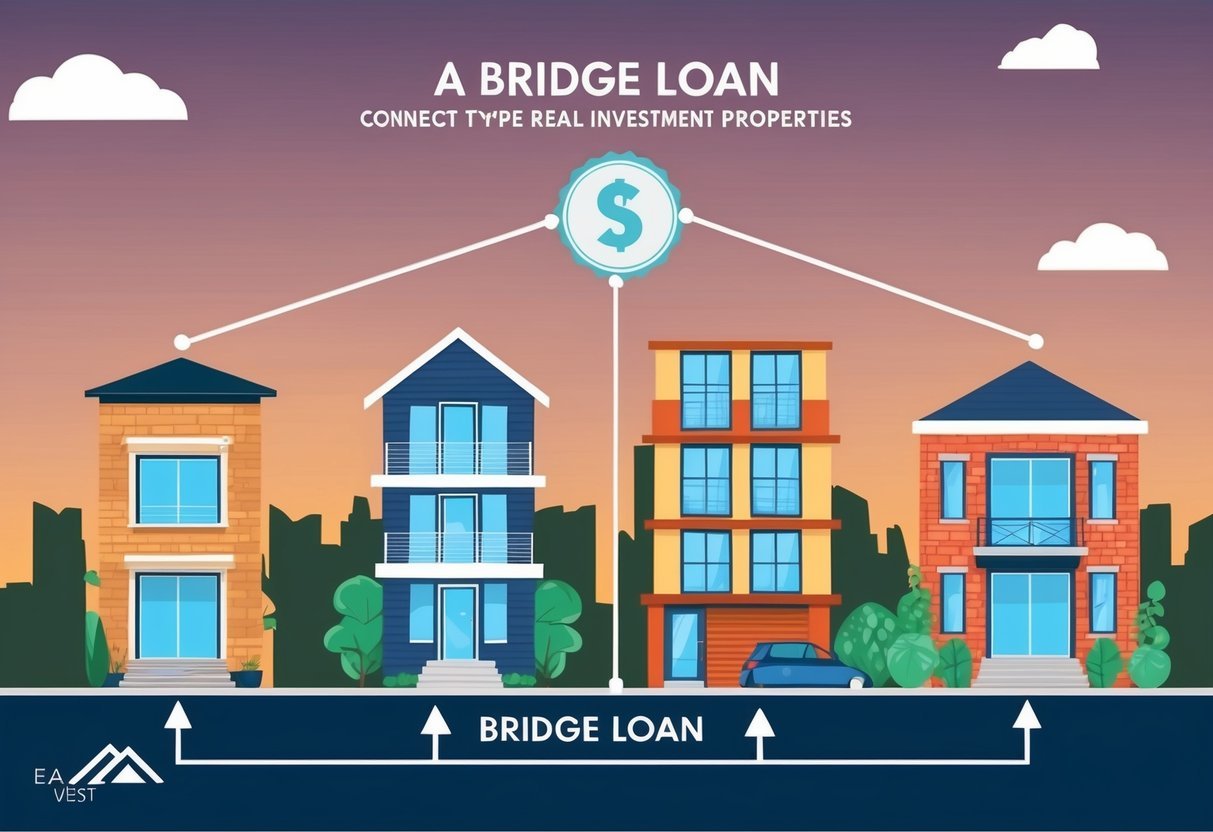

4) Bridge Loan

Bridge loans are a key tool for real estate investors seeking short-term financing solutions.

These loans help us seamlessly transition between property transactions, providing quick capital to close deals while we arrange for long-term financing.

In real estate, time is often of the essence.

Bridge loans allow us to act swiftly, securing properties that might otherwise slip away.

They are typically short-term, with repayment expected within 12 to 24 months.

This quick turnaround helps us maintain momentum in our investment strategies.

Bridge loans can also be used to finance renovations or repairs on a property before it’s ready for traditional financing or sale.

This flexibility allows us to add value to our investments, enhancing potential returns when the property is sold or refinanced.

These loans are generally secured against an existing property, leveraging its equity to fund new opportunities.

As a result, they require thorough assessment of our current holdings to ensure the risk is manageable and aligns with our investment goals.

While bridge loans offer numerous advantages, they typically come with higher interest rates and fees compared to traditional financing.

This is the trade-off for the speed and flexibility they provide.

Careful planning and analysis are crucial to ensure that the benefits outweigh the costs.

Understanding the 4 Types of Loans

When investing in real estate, understanding the different loan types is crucial.

Each type serves specific scenarios and offers various benefits and challenges.

1.

Conventional Loans: These are popular choices for real estate investors.

They usually have fixed interest rates and require substantial down payments. Conforming loans fall within limits set by Fannie Mae and Freddie Mac, while non-conforming loans exceed these limits.

2.

FHA Loans: Ideal for those starting in real estate investing, FHA loans feature low down payment requirements.

Although they come with mortgage insurance premiums, their flexibility often attracts first-time investors.

3.

Commercial Loans: Used for properties like office spaces, retail, or multi-family units.

These loans typically have higher down payment requirements and shorter repayment terms.

The interest rates vary according to creditworthiness and market conditions.

4.

Hard Money Loans: These are short-term loans often used by flippers.

They offer quick financing based on property value rather than creditworthiness.

Though convenient, they come with higher interest rates and fees.

Each type of loan has its own unique characteristics and is suited to different investment strategies.

Understanding these options allows us to make informed decisions based on our goals and financial profiles.

Eligibility Criteria for Real Estate Investment Loans

When securing financing for real estate investment properties, potential borrowers face certain criteria.

Key factors include credit score benchmarks, proof of income, and down payment amounts.

These aspects ensure lenders that borrowers are capable of managing and repaying the loan.

Credit Score Requirements

Lenders rely heavily on credit scores to assess risk.

For real estate investment loans, a minimum credit score of 620 is typically required.

Higher scores often favor better interest rates and terms.

We strive to maintain strong credit histories to improve our financing options.

Regularly reviewing and addressing credit reports can help correct discrepancies, which positively impacts our eligibility.

Income Verification

A stable income is crucial for loan approval.

Lenders require documentation such as W-2 forms, tax returns, and bank statements to verify our financial standing.

By providing comprehensive records, we demonstrate our ability to manage loan repayments.

For self-employed individuals, additional paperwork, such as profit and loss statements, might be necessary to support income claims.

Down Payment Requirements

Investment properties usually demand higher down payments compared to primary residences.

A minimum down payment of 15% is common, but 20% or more might enhance our loan terms.

A larger down payment reduces the lender’s risk, potentially securing lower interest rates.

Therefore, our savings plan should include adequate funds to meet these requirements, allowing us to invest with confidence.

Benefits and Risks of Real Estate Investment Loans

Real estate investment loans offer powerful advantages for expanding our portfolio but come with potential risks that need careful consideration.

Let’s explore both sides to make informed financial decisions.

Advantages

Investment loans give us access to substantial capital for acquiring properties or even renovating existing ones.

This financing strategy is essential for growing our real estate portfolios, enabling us to invest in a diverse range of property types and locations. Increased leverage allows us to buy more assets with less personal investment, potentially amplifying returns.

Additionally, many of these loans come with flexible terms, allowing us to structure payments in a way that aligns with our investment strategy.

Some lenders offer rapid prequalification and approval processes, ensuring that we can act quickly in a competitive market. Tax benefits are another compelling advantage; interest payments on these loans can often be deducted, providing significant savings.

Potential Drawbacks

While real estate investment loans provide opportunities, they also carry certain risks. Market fluctuations can impact property values, possibly leading to a situation where the owed loan exceeds the asset value.

High leverage, though initially beneficial, can become a burden if the market declines or rental incomes dip.

Interest rates and associated costs can vary widely, and securing loans usually involves substantial closing costs, adding to the initial financial burden.

Furthermore, if we opt for short-term financing, balloon payments may come due at inopportune times, requiring strategic planning to manage.

Lastly, depending on our creditworthiness, loan terms might impose strict repayment conditions, affecting cash flow flexibility.

Tips for Choosing the Right Loan

When choosing a loan for real estate investments, make sure to align it with your specific objectives and carefully evaluate various loan conditions.

Key aspects include understanding your investment strategy and comparing terms across lenders.

Assessing Your Investment Goals

To choose the most suitable loan, you must first clarify your investment goals.

Are you looking for long-term rental income or short-term property flipping? Investment strategies influence loan choices significantly.

For longer-term investments, a fixed-rate mortgage might be preferable to ensure stability in monthly payments.

Knowing the duration of your investment is vital.

A property intended for quick resale requires different financing compared to a long-term hold.

Additionally, considering your risk tolerance helps determine the loan structure that fits your comfort level.

By focusing on your goals, you can select a loan that supports your financial strategy effectively.

Comparing Loan Terms

Comparing the terms of different loan options enables you to identify the right choice for your needs. Interest rates, down payment requirements, and loan duration are critical factors to examine.

A lower interest rate might seem attractive, but make sure to assess the total cost over the loan’s lifetime.

Pay attention to any additional fees or hidden costs that might not be immediately apparent.

Evaluating various lenders’ offers will require you to consider not just the immediate costs but the long-term financial implications as well.

It’s beneficial to consult a financial advisor to assist in comparing these factors, ensuring you make an informed decision.

Frequently Asked Questions

In this section, we address inquiries related to financing options, qualifications, and practical tips for real estate investment properties.

Learn about favorable loan terms and how leverage impacts your investments.

What are the common financing options available for real estate investment properties?

We often consider conventional loans, hard money loans, FHA 203(k) loans, and bridge loans as primary options.

Each type provides distinct advantages and caters to specific investment goals, enabling a diverse range of real estate opportunities.

How does one qualify for a loan on an investment property?

Qualifying usually entails having good to excellent credit and a low debt-to-income ratio.

Lenders typically require a substantial down payment, often 20% or more, to mitigate risk.

Satisfying these criteria positions you as a viable candidate for securing financing.

What loan terms are typically favorable for investment property financing?

Favorable loan terms often include competitive interest rates, extended repayment periods, and minimal fees.

These terms help you manage cash flow effectively and optimize your investment returns over time.

Can you acquire a rental property loan with no down payment, and if so, how?

You can acquire a rental property loan with no down payment through specific programs like HomeReady and Home Possible.

These initiatives may offer low down payment options, allowing you more flexibility when entering the real estate market.

What is a DSCR loan, and how does it pertain to rental properties?

A Debt Service Coverage Ratio (DSCR) loan assesses the property’s ability to cover debt obligations.

This type of loan focuses on the income generated by the property, providing an opportunity for you to leverage rental income in securing financing.

What are the implications of using leverage in real estate investment property financing?

Using leverage can enhance our purchasing power, enabling us to acquire more substantial investments.

It can amplify returns, but also carries increased risk.

It’s crucial we carefully balance leverage to avoid overextending finances.